Private wealth management and investment banking are two of the most prominent career paths in finance, yet they share almost nothing in common beyond the industry label. One is a relationship-driven business where you build a book over decades. The other is a transaction-driven business where you execute deals in intense sprints. Choosing between them, or understanding which one aligns with your strengths, requires an honest look at what each path actually entails.

What Each Role Actually Involves

Investment Banking

Investment bankers advise corporations on mergers, acquisitions, IPOs, debt issuances, and restructurings. The work is project-based and intense.

Daily reality at the Analyst/Associate level:

- Building financial models (DCFs, LBOs, accretion/dilution)

- Creating pitch books and client presentations

- Conducting industry and company research

- Managing due diligence processes

- Coordinating with legal, accounting, and other advisors

- Working 70-90+ hours per week during live deals

The career arc: Analyst (2 years) → Associate (3 years) → VP (3-4 years) → Director/SVP (2-3 years) → Managing Director. Most people exit after the Analyst or Associate stage for buy-side roles, corporate development, or other opportunities.

Private Wealth Management

PWM advisors manage investment portfolios and provide full financial planning for high-net-worth (HNW) and ultra-high-net-worth (UHNW) individuals and families.

Daily reality:

- Meeting with clients to discuss portfolio strategy, goals, and market outlook

- Building and rebalancing investment portfolios

- Coordinating with estate attorneys, tax advisors, and insurance specialists

- Prospecting and building your client book (especially in early years)

- Analyzing investment products, manager selection, and asset allocation

- Working 50-60 hours per week with control over your schedule

The career arc: Analyst/Associate → Financial Advisor / VP → Director → Managing Director / Team Lead. The trajectory is entrepreneurial, your advancement is tied to the size of your book, not a promotion committee.

Compensation: Short-Term vs Long-Term

This is where the conversation gets nuanced. IB pays more upfront. PWM can pay more over a full career, but only if you build a large book.

Early Career (Years 1-5)

| Level | Investment Banking | Private Wealth Management |

|---|---|---|

| Year 1 | $175-225K all-in | $80-130K all-in |

| Year 3 | $250-350K all-in | $100-200K all-in |

| Year 5 | $350-500K all-in (Associate) | $150-350K all-in |

IB dominates early-career compensation. There's no debate. A first-year IB analyst at a bulge bracket earns roughly double what a first-year PWM associate earns.

Mid-Career (Years 5-15)

| Level | Investment Banking | Private Wealth Management |

|---|---|---|

| Year 7 | $500-700K (VP) | $250-500K |

| Year 10 | $700K-1.2M (Director/SVP) | $400K-1M+ |

| Year 15 | $1M-3M+ (MD, if you make it) | $500K-3M+ |

The gap narrows significantly. A successful PWM advisor with $500M+ AUM can earn $1-3M+, which is comparable to an IB Managing Director. The difference is that ~30-40% of IB analysts who start will still be in banking at year 15, while a PWM advisor who builds a book owns an annuity-like revenue stream.

Senior / Peak Career (Years 15+)

| Level | Investment Banking | Private Wealth Management |

|---|---|---|

| Top performers | $3-10M+ (top MDs, group heads) | $3-10M+ (large team leads, $1B+ AUM) |

| Typical senior | $1-3M (average MD) | $1-5M (established advisors) |

At the peak, the ranges converge. Elite performers in both fields earn $5-10M+. The structural difference is that a PWM advisor's revenue is recurring (management fees on AUM), while an IB MD's compensation resets annually based on deal flow.

Get weekly finance recruiting intel

Technical prep tips, recruiting timeline updates, and career strategies. No spam.

No spam. Unsubscribe anytime.

Lifestyle Comparison

| Factor | Investment Banking | Private Wealth Management |

|---|---|---|

| Weekly hours | 70-90+ (Analyst/Associate) | 50-60 |

| Weekend work | Frequent and expected | Rare (occasional client events) |

| Schedule control | Minimal, deals dictate timing | High, you set meetings |

| Travel | Moderate (client meetings, roadshows) | Low-moderate (client visits) |

| Stress type | Execution pressure, tight deadlines | Business development pressure, markets |

| Burnout rate | Very high (most leave within 4-6 years) | Lower (career tenure is common) |

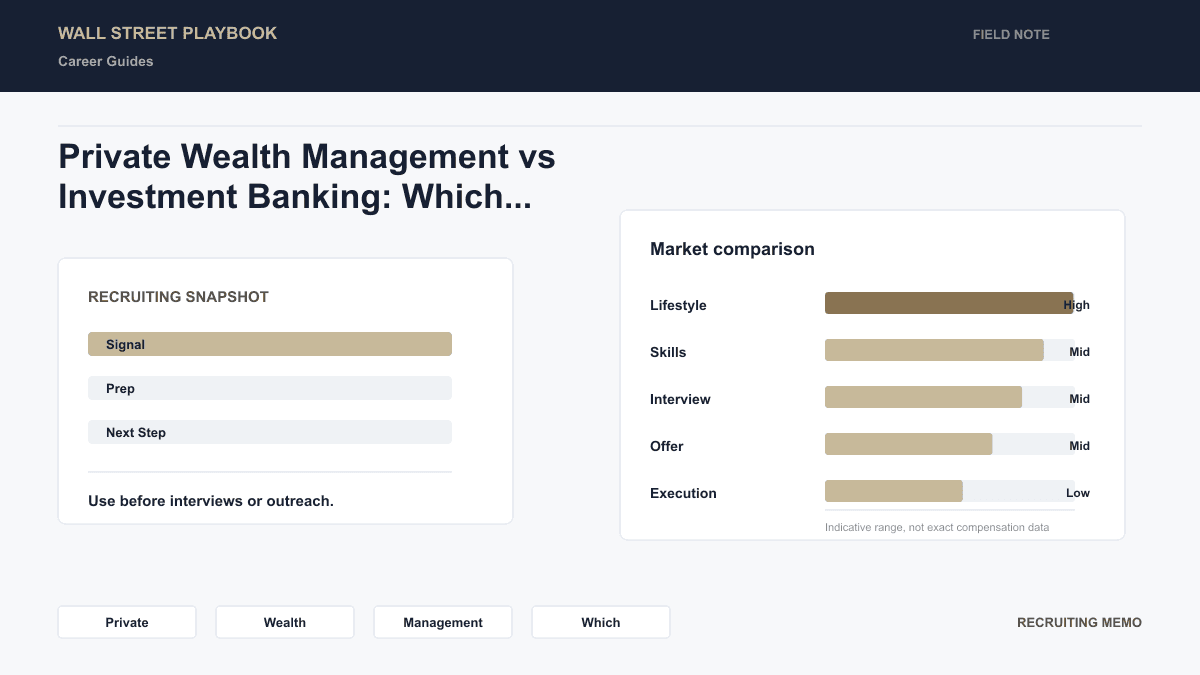

The lifestyle gap is not marginal, it's fundamental. IB is a young person's game structurally. PWM is designed for a 30-year career. If you're making a choice at 22, consider not just what you want now but what you want at 35 and 45.

Skills Required

Investment Banking

- Advanced financial modeling (DCF, LBO, M&A analysis)

- Attention to detail under extreme time pressure

- Ability to function on limited sleep

- Project management across multiple workstreams

- Polished client communication

Private Wealth Management

- Relationship building and trust development with affluent individuals

- Portfolio construction and investment knowledge

- Sales ability, especially the skill of prospecting without being pushy

- Holistic financial planning (tax, estate, insurance, philanthropy)

- Emotional intelligence for navigating personal and family financial dynamics

The skill profiles barely overlap. IB rewards technical precision and stamina. PWM rewards emotional intelligence and long-term relationship cultivation.

Exit Opportunities

From Investment Banking

IB is widely regarded as the strongest launchpad in finance:

- Private equity (on-cycle and off-cycle)

- Hedge funds

- Venture capital

- Corporate development

- Growth equity

- Operating roles at portfolio companies

The "exit opportunity" narrative is a core part of IB's value proposition. Many analysts enter banking explicitly to access these transitions.

Recommended Resource

How to Break Into Finance - 2026

110 pages. The recruiting system from first target list to signed offer.

From Private Wealth Management

PWM exits are more lateral than vertical:

- Family offices (SFO/MFO investment roles)

- RIA platforms and independent advisory firms

- Institutional asset management (client-facing roles)

- Private banking leadership

- Launching your own advisory practice

- Fintech and wealthtech companies

PWM doesn't open the same doors to PE or hedge fund investing that IB does. If buy-side investing is your end goal, IB is the better starting point. If client-facing advisory work is your calling, PWM gets you there faster and with less suffering.

Looking to position your resume for private wealth management roles? Our Resume Review Service helps you highlight the exact experience hiring managers look for.

Who Should Choose Which

Choose Investment Banking If You:

- Want maximum career optionality after 2-4 years

- Are targeting private equity, hedge funds, or buy-side investing

- Can tolerate (and even thrive in) 80-hour weeks for 2+ years

- Value prestige and brand signaling early in your career

- Don't mind that most people leave the field within 5 years

- Want high upfront compensation

Choose Private Wealth Management If You:

- Are drawn to building long-term client relationships

- Want to own a business within a business (your client book)

- Value schedule control and lifestyle sustainability

- Have strong interpersonal and emotional intelligence skills

- Want a career you can sustain for 25-30+ years

- Are comfortable with lower early compensation for potentially higher lifetime earnings

- Are entrepreneurial, PWM rewards those who can develop business

The Overlooked Advantages of PWM

The finance community disproportionately values IB, and some of PWM's real strengths get buried:

Ownership economics. A PWM advisor with a $1B book generating 50-70 bps in revenue has a $5-7M annual revenue stream. That's a small business with extraordinarily high margins. When you retire or sell your book, you capture 2-3x trailing revenue, effectively a multi-million-dollar exit.

Compounding relationships. Client relationships in PWM compound over decades. Your best clients refer their children, their friends, their business partners. IB relationships are transactional, each deal is a discrete engagement.

Intellectual breadth. Top PWM advisors understand investing, tax planning, estate law, insurance, philanthropy, and behavioral finance. The role is genuinely multidisciplinary.

The Bottom Line

Investment banking is the better choice for those who want a 2-4 year high-intensity experience that maximizes future optionality, especially toward buy-side investing. Private wealth management is the better choice for those who want to build an enduring, client-centric career with compounding economics and sustainable lifestyle.

Neither path is universally superior. The right choice depends on your temperament, timeline, and what you actually want your days to look like, not just your compensation.

Related Reading

- Bulge Bracket Investment Banking Salary 2026, What IB analysts and associates actually earn

- Working at a Family Office: What It's Actually Like, Another client-adjacent career path

- Non-Target to Investment Banking: Complete Playbook, Breaking into IB from a non-traditional background

- How Finance Jobs Are Actually Filled in 2026, Understanding the hidden job market for both paths