Private credit and private equity both sit under the alternatives umbrella, but they are fundamentally different businesses. One underwrites risk through the capital structure. The other takes ownership stakes and drives value creation. The confusion persists because both recruit from investment banking, both target middle-market companies, and both sit inside the same multi-strategy platforms.

This guide breaks down the real differences—so you can make an informed career decision rather than defaulting to whichever offer lands first.

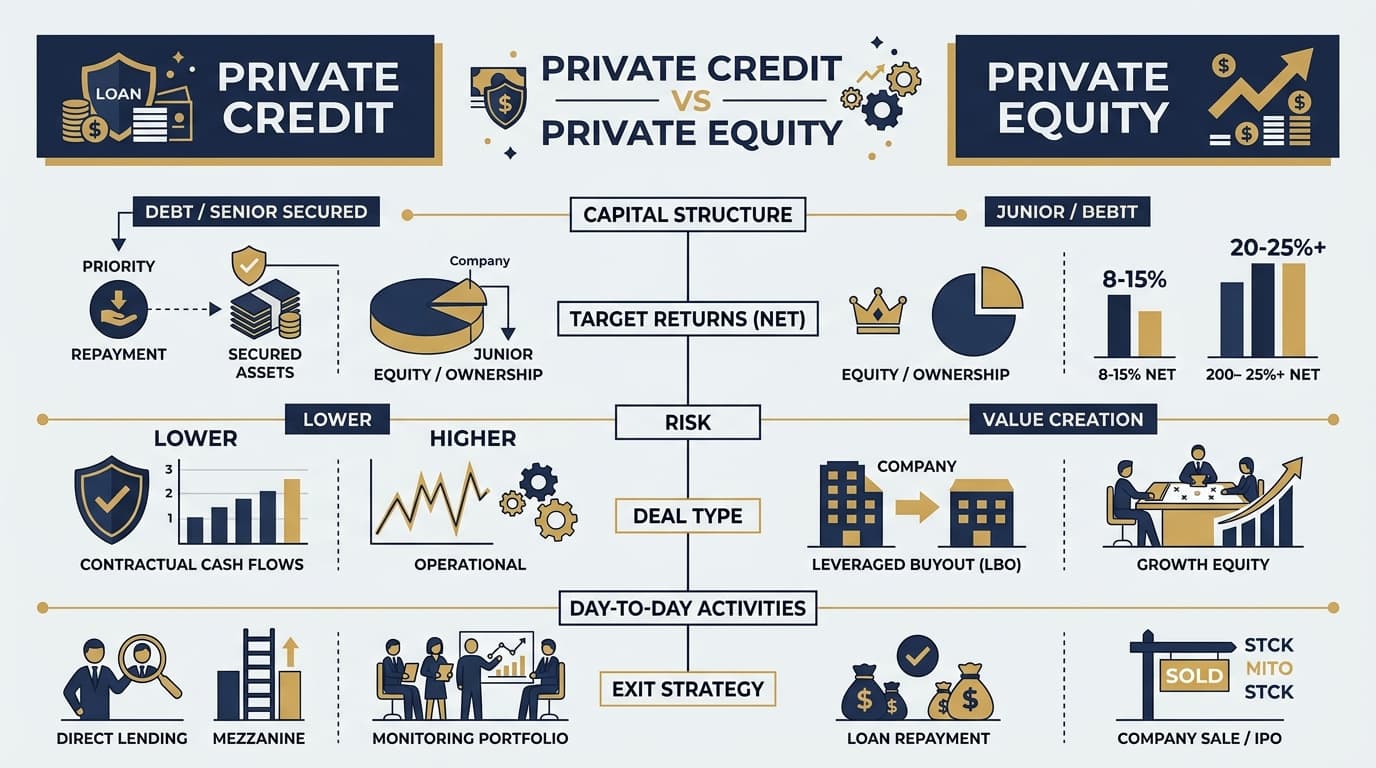

What Each Side Actually Does

Private credit (also called direct lending, private debt, or alternative credit) provides loans directly to companies, bypassing traditional banks. These are typically senior secured, unitranche, or mezzanine loans to sponsor-backed or non-sponsor middle-market companies. The fund earns a fixed or floating-rate coupon plus origination fees. You're underwriting downside risk—your primary question is "will this company repay?"

Private equity acquires controlling or significant minority stakes in companies, then works to increase enterprise value over a 3-7 year hold period through operational improvements, revenue growth, multiple expansion, or financial engineering. Your primary question is "how much more can this business be worth?"

Deal Types and Capital Structure Position

| Feature | Private Credit | Private Equity |

|---|---|---|

| Capital structure | Senior debt, unitranche, mezzanine, second lien | Equity (common + preferred) |

| Typical deal size | $50M-$500M loan commitments | $100M-$5B+ enterprise value |

| Return target | 8-15% gross (yield + fees) | 20-30%+ gross IRR |

| Downside exposure | Principal loss only if company defaults | Total loss of equity possible |

| Upside participation | Capped (occasionally with equity kickers/warrants) | Uncapped |

| Hold period | 3-7 years (floating, can repay early) | 3-7 years (exit via sale or IPO) |

| Deal volume per year | 15-40+ deals reviewed, 8-15 closed | 50-100+ deals reviewed, 2-5 closed |

Private credit funds deploy capital much more frequently than PE funds. That higher velocity means more reps on credit analysis but shallower involvement per deal.

Day-to-Day Work Compared

Private Credit Analyst/Associate

- Credit memos analyzing borrower financials, industry dynamics, and downside scenarios

- Financial modeling focused on debt service coverage, leverage ratios, and recovery analysis

- Portfolio monitoring—reviewing quarterly financials, covenant compliance, amendment requests

- Structuring terms (covenants, pricing, amortization, call protection)

- Relationship management with sponsors and borrowers

The rhythm is steadier. You'll work on multiple live deals simultaneously, and the portfolio monitoring component means a constant flow of existing credits to track.

Get the paper LBO template

Download the free template and use it alongside your PE interview prep.

No spam. Unsubscribe anytime.

Private Equity Associate

- Detailed LBO modeling, operating builds, and scenario analysis

- Due diligence deep dives—commercial, operational, financial, legal

- Management meetings and industry expert calls

- Portfolio company board materials and strategic projects

- Deal sourcing and thesis development

PE work comes in intense waves. You might spend two months on a single deal with 80+ hour weeks during diligence, then shift to portfolio work or sourcing during quieter stretches.

Compensation Comparison (2026)

| Level | Private Credit | Private Equity (MM-UMM) |

|---|---|---|

| Analyst/Associate Year 1 | $200-300K all-in | $250-400K all-in |

| Senior Associate / VP | $350-550K all-in | $450-700K all-in |

| Director / Principal | $500K-1M+ | $700K-1.2M+ |

| Managing Director / Partner | $1M-3M+ | $1.5M-5M+ (carry-dependent) |

PE compensation is higher at every level, but the gap narrows when you factor in carry timing. Credit fund carry (where it exists) vests faster because deals exit more frequently through refinancings and repayments. PE carry is larger but can take a decade to fully realize.

The lifestyle premium in credit is real. Most credit professionals work 50-60 hour weeks. PE associates routinely hit 65-80+.

Risk/Reward Profile for Your Career

Private credit offers:

- More predictable hours and career progression

- Faster path to portfolio responsibility

- Lower compensation ceiling but steadier trajectory

- Growing AUM—private credit has nearly tripled since 2018

- Less "up or out" pressure than PE

Private equity offers:

- Higher peak compensation through carried interest

- Broader strategic and operational skill development

- Stronger brand signaling for future opportunities

- More exit optionality (operating roles, hedge funds, VC)

- Tournament-style promotion path with higher attrition

Recommended Resource

2026 PE Recruiting Playbook

42 pages. Headhunter intel, timelines, compensation data, and PE interview frameworks.

Recruiting Paths

Both recruit from investment banking analyst programs, but the pipelines differ.

Private credit recruiting is less structured than PE. Many credit funds recruit on a rolling basis rather than through on-cycle processes. Lateral hires from leveraged finance, restructuring, and ratings agencies are common. The interview process emphasizes credit judgment—expect case studies around lending decisions, covenant analysis, and distressed scenarios.

Private equity recruiting remains dominated by on-cycle headhunter processes at the megafund and upper-middle-market level. Technical interviews are more intensive, with LBO modeling tests, deal walkthroughs, and case studies being standard.

One underappreciated difference: private credit is significantly easier to break into laterally. If you're 2-4 years into your career and didn't recruit for PE on-cycle, credit funds are far more accessible.

Looking to position your resume for private credit roles? Our Resume Review Service helps you highlight the exact experience hiring managers look for.

Which Should You Choose?

Choose private credit if you:

- Value predictable hours and sustainable lifestyle

- Are drawn to analytical credit work over operational value creation

- Want faster deployment of capital and more deal reps

- Are comfortable with a lower (but growing) compensation ceiling

- Want to build toward a portfolio manager seat

Choose private equity if you:

- Want the highest possible long-term compensation

- Thrive in high-intensity, deal-driven environments

- Want broad exposure to operations, strategy, and governance

- Are comfortable with an "up or out" tournament dynamic

- Value optionality for post-PE careers

The Bottom Line

Private credit is not "PE lite." It's a distinct asset class with its own skill set, career trajectory, and reward structure. The sector has grown from a niche corner of alternatives to a $1.7 trillion market, and the talent demand reflects that.

PE still commands the most prestige in recruiting circles, but prestige doesn't pay your rent—compensation, career durability, and personal fit do. Both paths lead to genuinely rewarding careers in finance. The right choice depends on what you optimize for.

Related Reading

- PE Compensation 2026: What Associates Actually Make — Detailed PE comp data by level and fund tier

- PE On-Cycle Recruiting 2026: Prep Guide & Timeline — The full on-cycle preparation checklist

- Elite Boutique Investment Banking Salary 2026 — Where bankers start before making the jump