Fund of funds (FoF) sits at the intersection of investing and talent evaluation. Instead of picking stocks or buying companies, you're picking the people who pick stocks and buy companies. It's a meta-investment role that rewards judgment, pattern recognition, and the ability to separate genuine skill from luck—or good marketing.

Despite managing trillions in capital globally, the FoF and allocator world remains poorly understood by most finance candidates. This guide explains what the job actually involves, what it pays, and whether it's the right path for you.

What Fund of Funds Analysts Actually Do

A FoF analyst's core job is evaluating external investment managers—hedge funds, private equity funds, venture capital, real assets—and recommending allocations to the portfolio.

The daily workflow:

- Manager sourcing: Identifying new funds through databases (PitchBook, Preqin, eVestment), conferences, and industry relationships

- Quantitative screening: Analyzing track records, risk metrics, attribution data, and peer comparisons

- Qualitative due diligence: Meeting with portfolio managers and their teams to assess investment process, organizational stability, and edge sustainability

- Operational due diligence: Evaluating fund infrastructure—administrators, auditors, compliance, valuation policies, counterparty risk

- Investment committee memos: Writing detailed recommendations that synthesize quantitative and qualitative findings

- Portfolio monitoring: Tracking existing allocations, reviewing quarterly letters, attending annual meetings, and flagging concerns

- Portfolio construction: Working with senior team members on asset allocation, liquidity management, and risk budgeting

You'll spend significant time in meetings—both on-site visits to managers and internal investment committee discussions. Travel is common, particularly for private markets due diligence that requires visiting portfolio companies and meeting operating teams.

Types of FoF and Allocator Platforms

| Platform Type | AUM Range | Focus | Example Firms |

|---|---|---|---|

| Institutional FoF | $5-50B+ | Multi-strategy, multi-asset class | Grosvenor, PAAMCO Prisma, K2 Advisors |

| Pension / Endowment | $1-500B+ | Full asset allocation | CalPERS, Yale Endowment, OTPP |

| Sovereign Wealth Fund | $10-1T+ | Cross-border, multi-asset | GIC, ADIA, Norges |

| Private Bank / Wealth Platform | $10-200B+ | Client-facing allocation | Goldman Sachs AWM, JPM AI |

| Specialized FoF | $500M-10B | Single asset class (HF, PE, VC) | Adams Street, Hamilton Lane, Aksia |

The role varies meaningfully by platform. At a pension fund, you'll cover 2-3 asset classes and focus on long-term strategic allocation. At a specialized hedge fund FoF, you'll go deep on 50-100 managers within a single strategy.

Skills That Matter Most

Analytical Skills

- Statistical analysis of track records (understanding Sharpe ratios, drawdowns, factor exposures)

- Financial modeling for private markets (fund cash flow modeling, J-curve analysis)

- Ability to parse marketing materials and identify genuine alpha versus beta or leverage

Judgment and Pattern Recognition

This is what separates great allocators from average ones. After meeting hundreds of managers, you develop intuition for:

- Which investment processes are repeatable versus one-time

- Whether a team has genuine edge or is riding market beta

- Organizational red flags (key-person risk, style drift, operational weaknesses)

- When strong recent performance masks deteriorating fundamentals

Get weekly finance recruiting intel

Technical prep tips, recruiting timeline updates, and career strategies. No spam.

No spam. Unsubscribe anytime.

Communication and Relationship Skills

You're meeting with some of the most sophisticated investors in the world—hedge fund PMs, PE partners, venture capitalists. You need to ask incisive questions, build genuine relationships, and represent your platform credibly.

Intellectual Breadth

FoF analysts must understand multiple asset classes, strategies, and market environments. You can't be an effective allocator to macro hedge funds if you don't understand rates markets, or to PE funds if you can't read an LBO model.

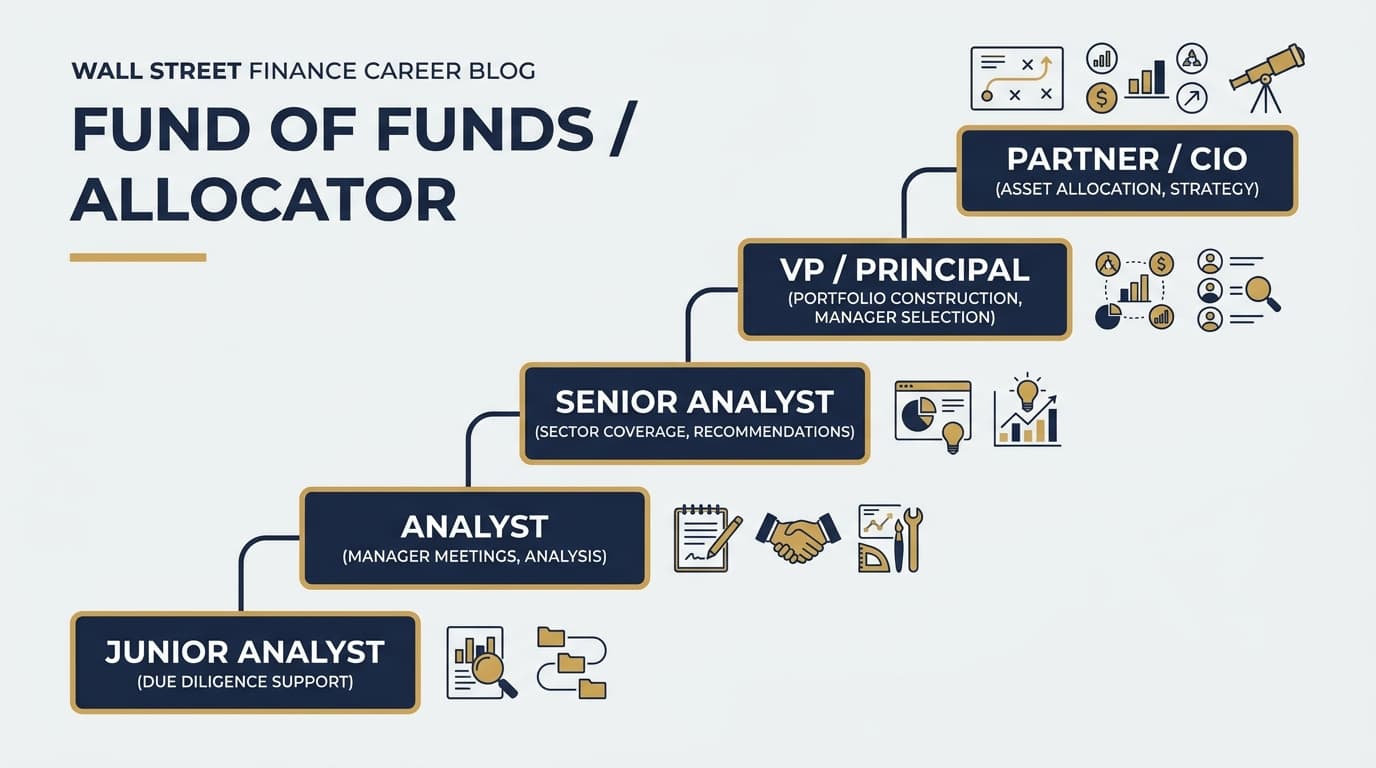

Career Progression and Compensation

| Level | Years | Typical Comp | Key Responsibility |

|---|---|---|---|

| Analyst | 0-3 | $100-175K | Screening, data analysis, memo support |

| Senior Analyst | 3-6 | $175-300K | Lead coverage of managers, IC presentations |

| Vice President | 6-10 | $300-500K | Sector/strategy lead, portfolio input |

| Director / Principal | 10-15 | $500K-1M | Investment committee member, allocation decisions |

| CIO / Partner | 15+ | $1M-5M+ | Portfolio-level responsibility, client relationships |

Compensation context: FoF compensation trails direct investing (PE, hedge funds) at every level. A VP at a PE fund earns $500-700K+; a VP at a FoF earns $300-500K. The gap widens at senior levels because FoF professionals don't receive carried interest on the same terms as GPs.

However, the lifestyle is notably better. FoF roles typically involve 50-55 hour weeks, reasonable travel schedules, and significantly less deal-driven stress than PE or hedge fund positions.

GP Side vs LP Side: Understanding the Divide

The finance industry has a fundamental divide between GPs (general partners—the people who manage money) and LPs (limited partners—the people who allocate to managers). FoF analysts sit on the LP side.

Advantages of the LP side:

- Panoramic view of the investment landscape across strategies and managers

- Relationship access to top-tier fund managers

- More sustainable pace and work-life balance

- Intellectually diverse—you're not trapped in one strategy or sector

Disadvantages of the LP side:

- Lower compensation ceiling than GP roles

- Less direct involvement in investment decisions (you pick managers, not securities)

- Can feel removed from "real" investing—you're evaluating rather than executing

- Perceived as less prestigious by some in the finance community

The transition question: Moving from LP to GP is possible but difficult. Allocators who want to transition to direct investing typically do so early in their careers (within 3-5 years). After a decade on the LP side, the transition becomes rare because your skill set has diverged significantly from what direct investment roles require.

Looking to position your resume for fund of funds and allocator roles? Our Resume Review Service helps you highlight the exact experience hiring managers look for.

Recommended Resource

How to Break Into Finance - 2026

110 pages. The recruiting system from first target list to signed offer.

How to Break In

Common entry paths:

- Investment banking analyst programs (2-year stint, then lateral)

- Investment consulting firms (Cambridge Associates, Mercer, Aon)

- Private bank analyst programs (Goldman Sachs, Morgan Stanley, JPM)

- Asset management rotational programs

- Direct from undergrad at some institutional allocators

What allocator firms look for:

- Intellectual curiosity across asset classes

- Strong written communication (memos are the primary deliverable)

- Quantitative comfort without being purely quantitative

- Genuine interest in manager evaluation and portfolio construction

- CFA progress (strongly preferred at most institutional allocators)

Who Should Consider This Path?

It's a strong fit if you:

- Are genuinely curious about how different investment strategies work

- Enjoy meeting people, building relationships, and evaluating talent

- Value breadth over depth in your investment knowledge

- Want a sustainable career with solid (if not peak) compensation

- See yourself as a judge of process rather than a generator of ideas

It's a poor fit if you:

- Want to be the one making investment decisions on specific securities

- Optimize primarily for compensation

- Find manager meetings and due diligence processes tedious

- Prefer deep specialization in one asset class or strategy

The Bottom Line

Fund of funds and allocator roles offer one of the most intellectually stimulating and lifestyle-friendly career paths in finance. You'll develop a breadth of investment knowledge that few other roles provide, build relationships across the industry, and contribute to capital allocation decisions that move billions.

The trade-off is clear: lower compensation and less direct involvement in investment execution. For those who value pattern recognition over security selection and breadth over depth, it's a deeply rewarding career.

Related Reading

- Portfolio Manager Career Path: From Analyst to PM — The buy-side PM trajectory compared

- Working at a Family Office: What It's Actually Like — Another alternative path in institutional investing

- Private Credit vs Private Equity: Key Differences in 2026 — Understanding the GP-side alternatives